Most UK students run out of money before the end of term-not because they’re spending too much on takeaways, but because they’re not tracking where it all goes. You get your maintenance loan, maybe a bit from parents, a part-time job paycheck, and suddenly it’s mid-February and you’re eating pasta three times a week. What if you could make every pound work for you? That’s the idea behind zero-based budgeting: no money sits idle. Every pound has a job. And yes, it works even if you’re on £800 a month.

What Zero-Based Budgeting Actually Means

Zero-based budgeting isn’t about cutting back-it’s about owning every pound. Unlike traditional budgeting where you say, “I’ll save what’s left,” zero-based budgeting says, “I’ll assign every pound before I even see it.” At the end of the month, your balance should be £0. Not because you’re broke, but because you’ve planned for everything: rent, food, bus fare, phone bill, even that £10 you want to spend on a gig.

This method was popularised by Dave Ramsey in the US, but it’s perfect for UK students because it forces you to match income with expenses exactly. No guesswork. No “I’ll figure it out later.” You decide where every penny goes-before you spend it.

Step 1: List All Your Income Sources

Start by writing down every single pound you expect to receive each month. Don’t leave anything out. Most UK students have:

- Student Finance England/Student Awards Agency Scotland (SAAS)/Student Finance Wales maintenance loan (paid in three instalments)

- Part-time job earnings (university job, bar work, tutoring)

- Occasional cash from family

- Side gigs (eBay, Fiverr, campus photography)

- Scholarships or bursaries (if applicable)

Let’s say your monthly income is £850: £700 from your loan, £100 from weekend shifts, and £50 from tutoring. That’s your total. Write it down. Now, don’t touch it yet. You’re not spending it-you’re assigning it.

Step 2: List Every Single Expense

Now list every cost you have. Be specific. Don’t just write “food.” Write “groceries,” “coffee out,” “takeaway once a week.” Don’t skip small stuff. A £3 daily coffee adds up to £90 a month. That’s a train ticket to London.

Here’s what a real student budget might look like:

- Rent: £450

- Utilities (gas, electricity, water): £40

- Internet: £20

- Phone bill: £15

- Groceries: £120

- Coffee & snacks: £30

- Transport (bus/train): £50

- Textbooks & supplies: £25

- Entertainment (cinema, gigs, nights out): £40

- Savings buffer (for emergencies): £20

- Personal care (toiletries, haircuts): £15

Total: £850. Exactly your income. That’s zero-based budgeting.

Step 3: Assign Every Pound Before You Spend It

Now, you need to assign each pound to a category. You can do this on paper, in Excel, or using a free app like Yolt or Monzo (both work well in the UK). The key is to move money into categories before you spend it.

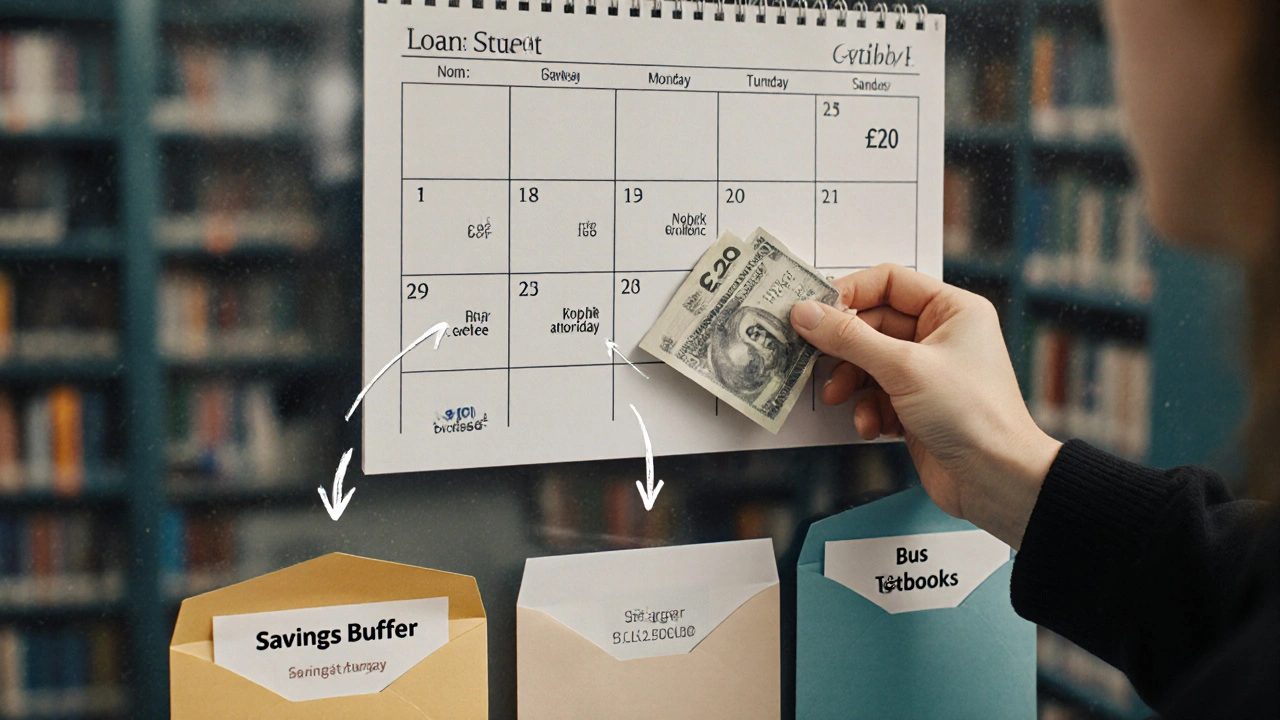

When your loan hits your account, don’t just leave it there. Immediately move:

- £450 to rent (set up a direct debit)

- £40 to utilities (auto-pay if possible)

- £20 to internet

- £15 to phone

- £120 to groceries (transfer to a separate savings pot)

- £30 to coffee/snacks

- £50 to transport

- £25 to textbooks

- £40 to entertainment

- £20 to savings

- £15 to personal care

Now your main account is empty. You’re not “waiting to spend.” You’ve already spent it-in your mind. When you go to buy groceries, you’re not dipping into your loan balance. You’re using the £120 you already set aside. That’s the power of zero-based budgeting.

Step 4: Track Every Purchase

At the end of each day, log every expense. Even if you bought a £1.50 chocolate bar. Use your bank app’s categorisation feature or a simple notebook. If you spent £5 on coffee instead of £3, you need to take £2 from another category. Maybe you cut your entertainment budget by £2 this week.

There’s no penalty for going over. You just rebalance. That’s the whole point. Budgets aren’t rules-they’re tools. If you go over on food, you take from entertainment. No guilt. No panic. Just adjustment.

Step 5: Build in Flexibility

Things happen. Your bus gets cancelled. Your laptop breaks. Your friend’s birthday is next week. That’s why you have a £20 buffer. Use it. But when you do, replace it next month. That £20 isn’t “extra.” It’s insurance. And if you don’t use it, roll it into next month’s savings or fun money.

Some students find it helpful to have a “miscellaneous” category of £10-£20. It’s not a free pass-it’s a safety net. You name it, you fund it. And if you don’t use it, you keep it.

Why This Works Better Than Other Budgeting Methods

Traditional budgeting says: “Spend £600, save £200.” But what if you only made £700? You’re forced to skip savings. Zero-based budgeting says: “You have £700. Rent is £450. Food is £120. Transport is £50. That’s £620. You have £80 left. Where does it go?”

It forces you to make conscious choices. You can’t say, “I’ll save when I have more.” You decide right now: is that £80 for books, or for a weekend trip? You’re not hoping for discipline-you’re building it into your system.

And it works with irregular income. If you get paid £200 one week and £50 the next, you still assign every pound as it comes in. No waiting. No “I’ll budget later.”

Common Mistakes UK Students Make

Here’s what goes wrong-and how to fix it:

- “I forgot about my student loan fees.” Some loans have admin charges. Check your award letter. Include it.

- “I thought my rent included utilities.” It doesn’t. Always confirm. If it doesn’t, add £40-£60.

- “I didn’t account for term-time vs holiday.” Your loan is split into three payments. Your rent might be monthly. Make sure your budget aligns with when money arrives, not when bills are due.

- “I used my budget as a limit, not a plan.” A budget isn’t a cap. It’s a plan. If you underspend on food, don’t just keep the cash. Move it to savings or next month’s fun fund.

Tools That Help (Free & UK-Friendly)

You don’t need fancy software. Here’s what works for students:

- Monzo: Lets you create “pots” for each budget category. Automatically rounds up spending and moves change into savings.

- Yolt: Links all your accounts. Shows spending by category. Great for seeing where your money really goes.

- Google Sheets: Free, simple. Copy a zero-based budget template online (search “UK student zero-based budget template”).

- Notion: If you like custom dashboards, build your own. Add reminders for loan dates.

Don’t overcomplicate it. The goal isn’t to spend hours on apps. It’s to know where your money is at all times.

What Happens When You Stick With It

After three months, you’ll notice things:

- You stop worrying about money before payday.

- You can say “no” to expensive nights out without guilt-you’ve already planned your fun money.

- You might even start saving for next year’s travel, or a new laptop.

- You’ll understand your spending habits better than most adults.

One student I spoke to saved £400 over her second year just by shifting £10 from takeaways to savings each week. That’s a deposit on a train ticket home for Christmas. Or a new pair of winter boots. Or a textbook you actually need.

Zero-based budgeting doesn’t make you rich. It makes you in control. And for a UK student, that’s worth more than any loan.

Can I use zero-based budgeting if my income changes every month?

Yes. Zero-based budgeting works best with variable income. When you get paid, assign every pound immediately. If you earn £500 one month and £900 the next, adjust your categories accordingly. Use last month’s overspending to inform this month’s plan. The key is assigning money as you receive it, not waiting for a “stable” amount.

What if I run out of money before the end of the month?

It happens. Don’t panic. Look at your budget: which category did you overspend on? Take the extra from next month’s budget. If you spent £50 on coffee instead of £30, reduce next month’s entertainment or snacks by £20. Zero-based budgeting isn’t about perfection-it’s about awareness and adjustment. If you’re consistently running short, you may need to increase your income or reduce fixed costs like rent.

Do I need to use a budgeting app?

No. You can use pen and paper, a notebook, or a simple Excel sheet. Apps like Monzo or Yolt make it easier because they auto-categorise spending and show real-time balances. But the method works whether you’re tech-savvy or not. The only requirement is that you assign every pound before you spend it.

Is zero-based budgeting the same as envelope budgeting?

They’re similar. Envelope budgeting uses physical cash in labelled envelopes. Zero-based budgeting does the same thing digitally-you assign money to categories. The core idea is identical: every pound has a job. The difference is the tool. Digital tools give you more flexibility and tracking, but both methods teach the same discipline.

How long does it take to get good at zero-based budgeting?

Most students feel comfortable after two months. The first month is about learning where your money actually goes. The second month is about adjusting. By month three, you’ll know exactly how much you can spend on food, how much you need for transport, and how much you can save. It becomes second nature-like brushing your teeth.